Quick Insights into Housing Market Dynamics: 2021's Upsurge and 2022's Decline

Impact of Mortgage scheme in UK real estate market and observation of different indicators such as GDP, Inflation Rate, Inward F.D.I & public sector expenditure on unemployment benefits from 2017-2022

This article is also published on Maven Analytics

The UK government has announced the 2021 mortgage scheme as mentioned below:

“The scheme offers lenders the option to purchase a guarantee on mortgages where a borrower has a deposit of only 5%. The guarantee compensates mortgage lenders for a portion of net losses suffered in the event of repossession. The guarantee applies down to 80% of the purchase value of the guaranteed property covering 95% of these net losses. The lender therefore retains a 5% risk in the portion of losses covered by the guarantee. This ensures that the lender retains some risk in every loan they lend” (1).

After this scheme, a notable increase in the number of houses sold throughout the year 2021 has been observed as shown above.

Similarly, the inward foreign direct investment has also increased in 2021:

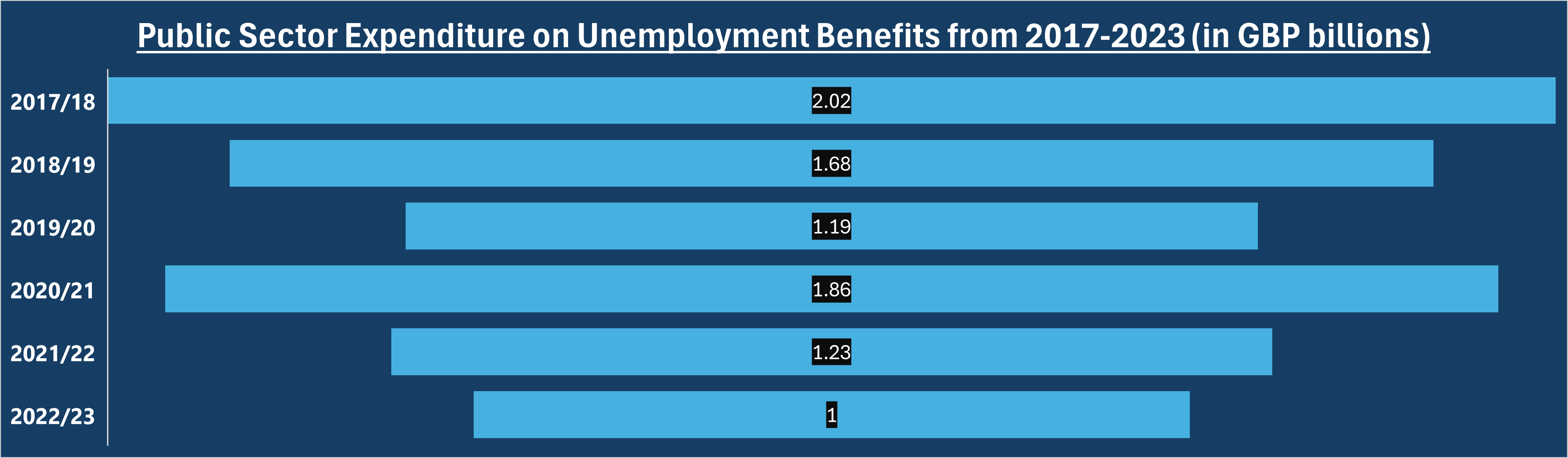

Despite experiencing a significant surge in 2021, housing sales witnessed a notable decline in 2022, even with the continued implementation of Mortgage scheme. This downturn may be attributed to the persistently high inflation rate, contributing to increased living costs in the UK. Additionally, the reduction in public sector expenditure on unemployment, hitting its lowest level since 2017 in 2022, could have further impacted the scheme's performance.

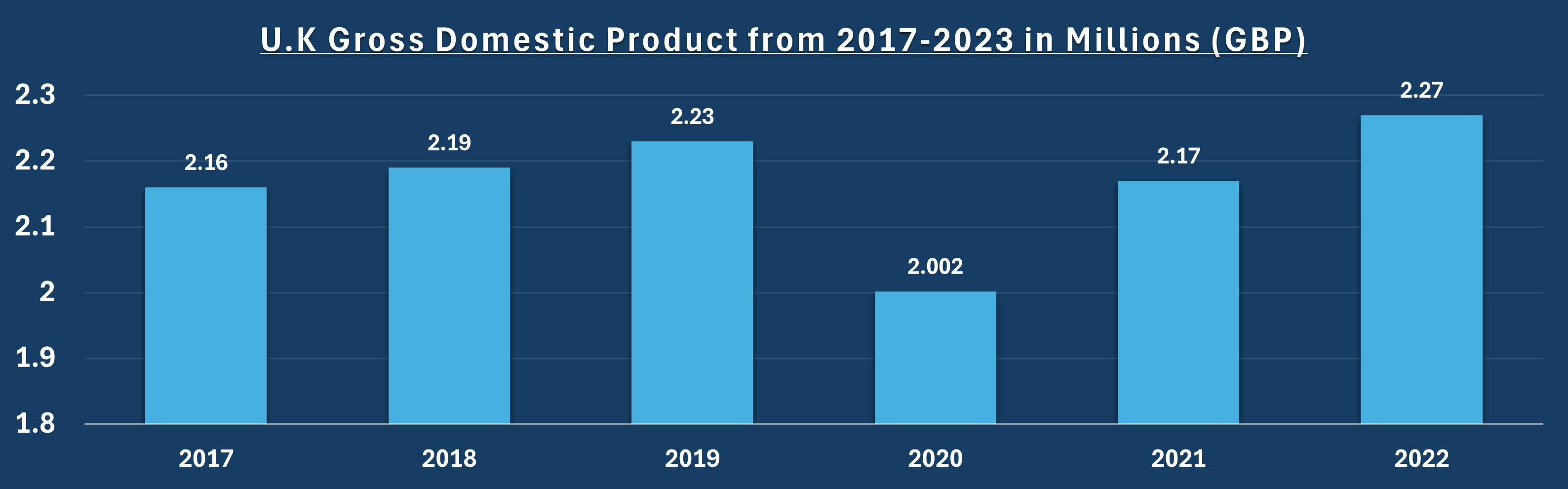

The GDP has grown to the highest level since 2017 but other factors have played a role in the year 2022 that has led to a decline in housing sales.

Thus, it becomes evident that there is a pressing need for the government to boost investment in public spending and implement strategies to counter inflation, aiming to foster growth within the real estate sector. GDP, often relied upon as an indicator, may not accurately reflect the dynamics of the real estate market.

References: